Is Interest Earned on an NRE Account Taxable in India? For Non-Resident Indians (NRIs), an NRE (Non-Resident External) Account is one of the most preferred banking options for managing income earned outside India. Apart from offering complete repatriability of funds, one of the biggest advantages of an NRE Account is the tax exemption available on […]

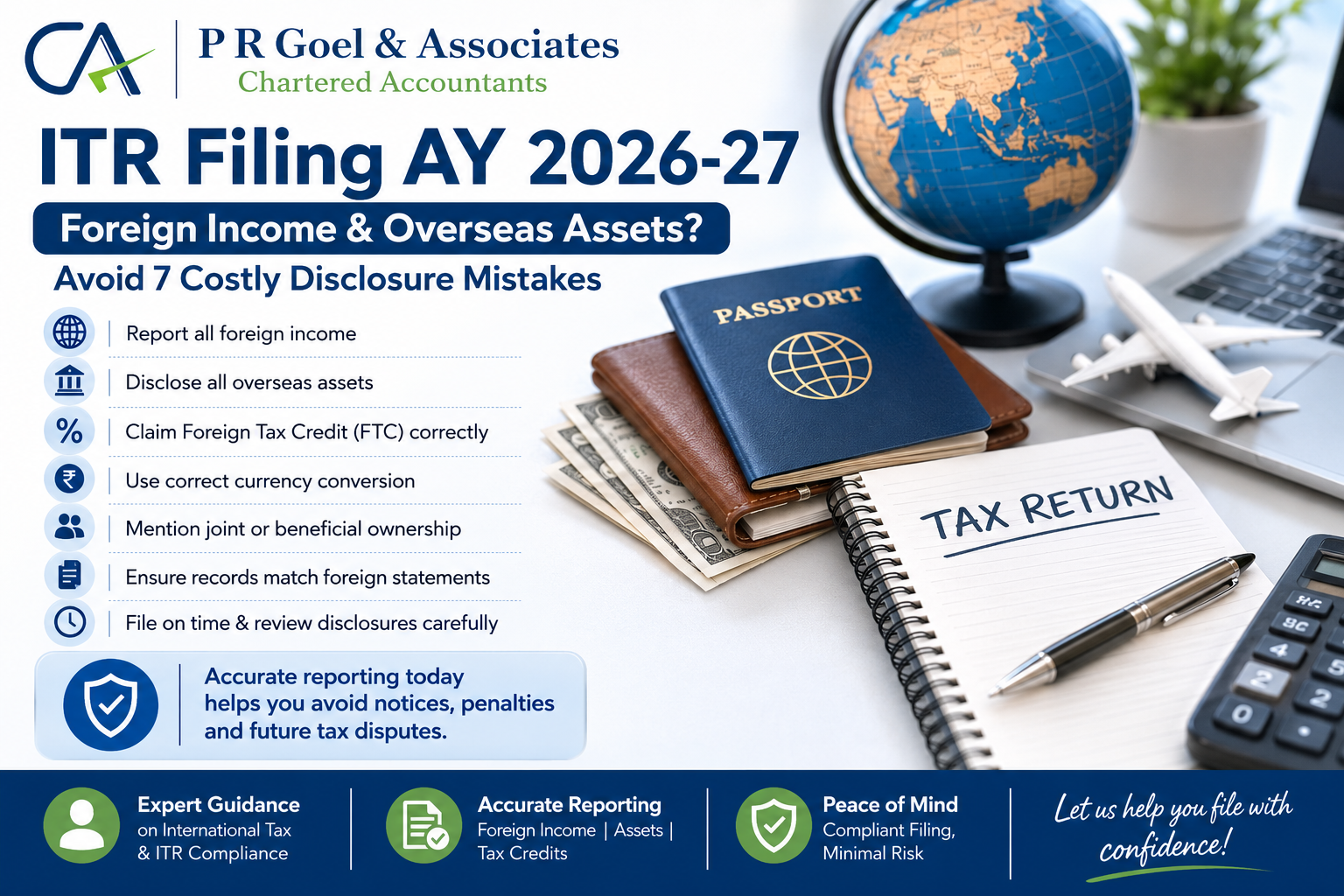

As global mobility increases, many Indian taxpayers earn income from overseas employment, foreign investments, rental properties, or hold bank accounts and financial assets outside India. While these opportunities bring financial benefits, they also come with additional tax reporting responsibilities under the Indian Income-tax Act. Failure to correctly disclose foreign income and overseas assets in your […]

Changing jobs can be a significant career milestone, but it can also make your Income Tax Return (ITR) filing more complicated. If you have worked with two or more employers during a financial year, overlooking certain tax implications can result in incorrect tax calculations, additional tax liability, notices from the Income Tax Department, or delayed […]